Discover Your Dream Career in UAE Hospitality

Find the latest jobs, walk-in interviews, salary insights, and career guidance for the UAE hospitality industry. Join thousands of professionals advancing their careers.

Featured Hospitality Jobs

Handpicked opportunities from top UAE employers

Waitress

Palma Beach Resort and Spa

Palma Beach Resort & Spa is dedicated to creating exceptional dining experiences in a beautiful ...

Housekeeping (HK) Supervisor

Luxe Hospitality

Housekeeping Supervisor Jobs in Dubai – Luxe Hotels Hiring NowLuxe Hotels is currently hiring an e...

Front Desk Agent

Copthorne Hotel Sharjah

? Front Desk Agent Jobs in Sharjah – Copthorne HotelCopthorne Hotel Sharjah, part of the prestigio...

F&B Service Staff

Barbeque Nation Restaurants LLC

? F&B Service Staff Jobs in UAE – Barbeque NationBarbeque Nation Restaurants LLC, a leading ca...

Cleaner

Katrina Sweets

? Cleaner Jobs in Dubai – Katrina SweetsKatrina Sweets is seeking reliable and detail-oriented Cle...

Barista

Katrina Sweets

? Barista Jobs in Dubai – Katrina SweetsKatrina Sweets is hiring skilled and customer-focused Bari...

Latest Career Resources

Stay updated with industry insights and advice

Apex Alwataniah Catering Walk-In Interview Dubai 2026 – Offshore Vacancies (7 February)

Apex Alwataniah Catering is conducting a walk-in interview in Dubai on 7 Februar...

Catering Assistant Interview Questions and Answers PDF – Free Guide for Freshers & Professionals

Prepare for your catering assistant interview with our complete guide. Get top i...

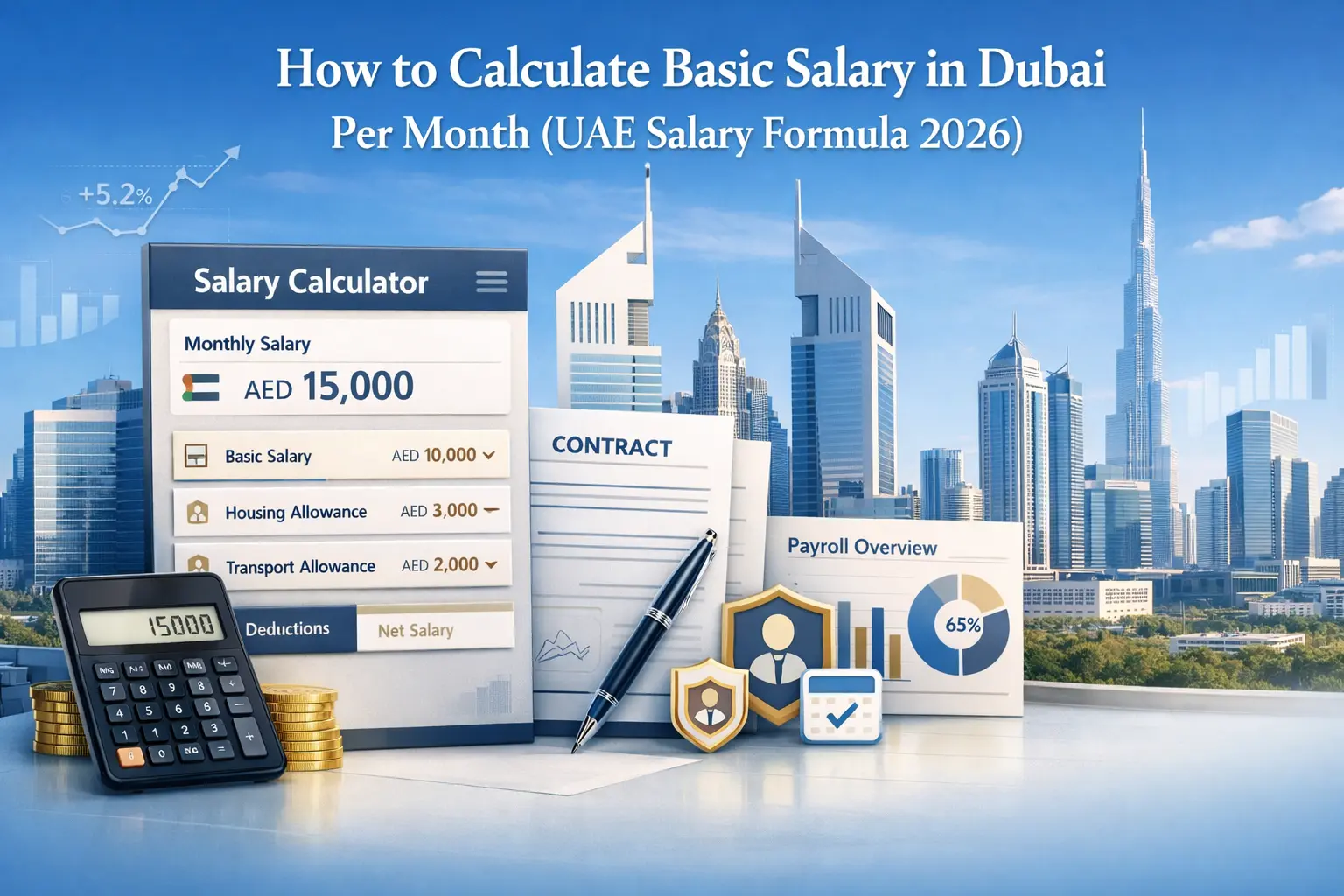

How to Calculate Basic Salary in Dubai Per Month (UAE Formula 2026)

Learn how to calculate basic salary in Dubai per month using UAE labour law. Det...

10 Cleaning Chemicals in Housekeeping (R1 to R9) – Complete Hotel Guide for UAE

Discover the complete list of 10 cleaning chemicals used in housekeeping, includ...

Explore Our Categories

Your complete career companion in UAE's hospitality sector

Why Choose UAEQuest.com?

The trusted platform for UAE hospitality professionals

Verified Employers

All companies are thoroughly vetted

Real-time Updates

Instant notifications for new opportunities

Career Guidance

Expert advice for career progression

Direct Applications

Apply directly to hiring managers

Salary Insights

Market salary data and trends

UAE Wide Coverage

Opportunities across all Emirates

Join Our Community

Connect with fellow hospitality professionals

Join Our WhatsApp Job Alert Group

Get instant notifications for walk-in interviews, urgent hiring, and latest job openings directly on WhatsApp.